Summer 2005

Summer 2005 |

|||||||

|

|

|||||||

2005/2010 Demographic Data Trends |

|||

|

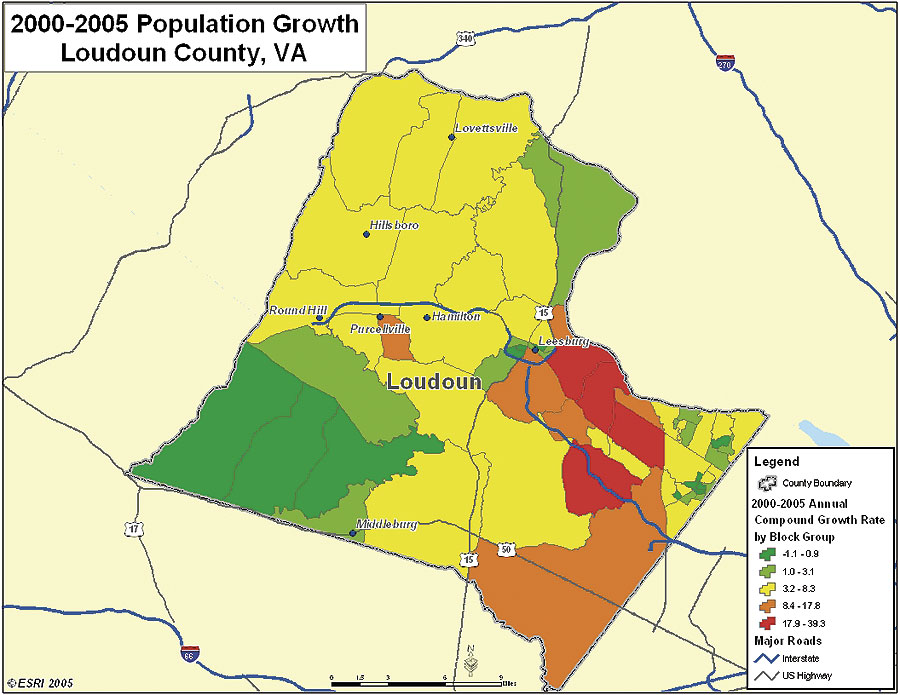

During the annual process of updating and forecasting demographic data, the Esri data development team noticed several significant trends in the demographics of the U.S. population. These trends reflect life in America today, and barring any unforeseen events, these trends are expected to continue for the next few years.

Approximately half the population in the United States—45 percent—is aged 40 years or older; most are "Baby Boomers." In 1950, shortly after the postwar baby boom began, approximately one in three Americans was 40 years old or older. The median age was declining; anyone over the age of 30 was considered old. Today, the median age is 36.3 years. By 2010, the median age will be 37.3 years, and the population in more than half the counties in the United States will reach a median age of more than 40 years. The baby boom shapes much more than the distribution of an aging population. This generation also represents 40 percent of the active labor force and more than half of all college graduates. Baby Boomer households control almost half the aggregate income in the United States and include 45 percent of all homeowners. The influence of this cohort extends well beyond its 26 percent share of the population. The generation that was disinclined to trust anyone over 30 is redefining the concept of seniority in America. The aging population is only half the picture. The growing diversification of the U.S. population through immigration is the counterforce in population change. The populations that are increasing through immigration are growing by 3 to 4 percent annually, led by growth in the Hispanic origin population. The Hispanic population has increased by 3.9 percent since 2000 to 14.5 percent of the U.S. population. Lagging slightly behind the Hispanic population growth, the Asian population is increasing by 3.7 percent annually. The lowest growth rate of 0.3 percent annually is evident in the non-Hispanic white population. Overall population growth through 2005 remains moderate at 1.1 percent annually. The most rapid growth is still found in the West at 1.6 percent and in the South at approximately 1.5 percent annually. In fact, most of the fastest growing counties in the country are in the southern or western states. Only 16 of the top 100 counties, ranked by population growth from 2000 through 2005, are located elsewhere (primarily in Minnesota). Most of the top 100 counties are growing by virtue of their proximity to a metropolitan area, such as Loudoun County, Virginia, the fastest-growing county in the United States. A suburb of the Washington, D.C., metropolitan area, Loudoun County now includes more than 250,000 people, increasing at an annual growth rate of more than 8 percent. Economic TrendsThe fastest-growing counties are generally not the wealthiest or the most expensive neighborhoods. Their common trait is location, usually in the fringe areas of major metropolitan centers. The wealthiest counties in the United States, measured by median household income, include more of the established suburbs in the Washington, D.C., metropolitan area and many California counties. Fairfax County, Virginia, maintains its number one position with the highest median household income in the country of more than $100,000. The 2005 median household income of the United States stands at $49,747, an annual increase of 3.2 percent since 2000. Average household income in 2005 exceeds $68,000. The most expensive neighborhoods in the United States, as measured by median home value, are predominantly found in California counties but still include some of the established neighborhoods on the eastern seaboard, especially in Massachusetts and New York. The year 2004 was another record breaker for appreciation in home value. Esri adjusted its 2005 estimate upward to accommodate the latest increase, although appreciation is expected to slow in the next few years. The median home value in 2005 is $163,247, an annual growth of 7.5 percent since 2000. California and the northeastern states continue to show double-digit appreciation in home value. Real estate values in Nevada followed suit, showing rapid appreciation in the past year to the current average of 11 percent. The gap between home value and income is widening, as indicated by the simple ratio between median home value and median household income. Affordable housing is becoming an issue, not only among lower income households. Although homeownership rates have increased, the strength of the real estate market includes the purchase of second homes, vacation homes, and investment property. According to the National Association of Realtors, these purchases account for nearly one-third of residential purchases. Favorable interest rates have facilitated an increase in home equity loans and refinancing activity, boosting cash available for spending. However, interest rates are also expected to continue rising. The era of easily available money appears to be coming to an end. The Federal Reserve Board is expected to increase the short-term federal fund rates steadily to 3 to 5 percent. While real Gross Domestic Product growth slowed to 3.9 percent in 2004 from 4.4 percent in the previous year, inflation as measured by the Consumer Price Index (CPI) is rising. In 2004, the average annual rate of inflation was 2.7 percent compared to 2.3 percent in 2003. The core CPI, which excludes the more volatile food and energy components, is also increasing. This is one of the indicators tracked by the Federal Reserve Board to measure inflationary pressures. Another indicator is productivity as measured by worker output per hour. Productivity declined in 2004 to 4 percent from 4.4 percent in 2003. Growth is expected to be slightly weaker in 2005 due in part to slowing productivity and relatively higher oil prices; however, the economic outlook also includes stronger job growth. Total employment has increased in 2005 to nearly 136.8 million jobs, a gain of 1.6 million over 2004. More than 85 percent of the employment gains occurred in the South and West. The rate of unemployment dropped slightly to 6.9 percent. Over the next five years, employment growth is expected to continue at about 1.5 percent annually, with a decrease in the unemployment rate to approximately 6 percent. What's New in 2005Here are some of the significant changes found in the 2005/2010 demographic data updates:

The 2005/2010 demographic data is available in Esri products, including hard-copy and online reports, printed sourcebooks, software, customized projects, and data licenses. For more information about Esri data products, visit www.esribis.com/data. |