Summer 2006

Summer 2006 |

|||||||

|

|

|||||||

2005–2015 NOAA International Remote-Sensing Research Report

Remote-Sensing Industry Strong and Growing over Next Decade |

|||||||||||

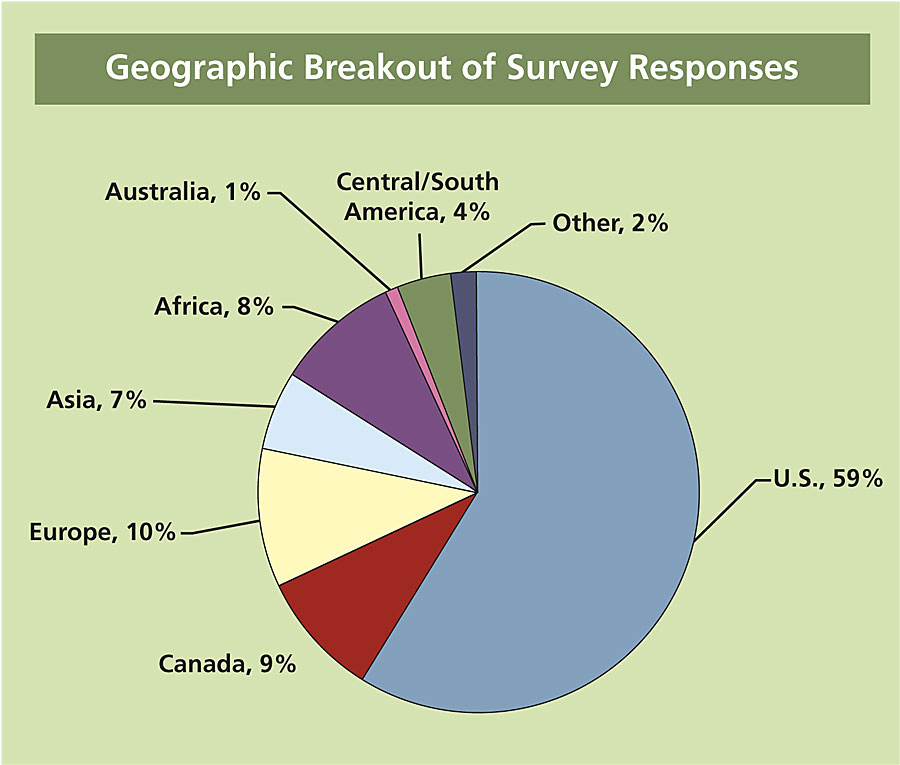

Conducted by the National Oceanic and Atmospheric Administration (NOAA), the study includes more than 1,500 online surveys and 250 personal interviews. The surveys and interviews provide a sample from the following eight remote sensing project sectors: Academic End Users, Aerial Digital, Aerial Film, Aerial Sensor, Commercial End User, Government End User, Satellite, and Software/Hardware Providers. Although the survey was focused on Canada, Europe, and the United States, the survey results also represented global input, with respondents from Africa, Asia, Australia, Central America, and South America. In addition to the remote-sensing technology data usage and budgetary data collected, this study also includes a 5- and 10-year analysis of the political, economic, and technical trends impacting the remote-sensing industry globally. These factors will shape the development of the industry by influencing end user demand for data, data availability, pricing, and applications. Technical, Environmental, Economic, and Political Trends Impact Industry DevelopmentAll of the respondents were asked to identify the technical advances they see impacting their businesses in the years 2010 and 2015. In 2010, Technology Integration, Greater Ground Resolution, and Greater Horizontal and Vertical Accuracy were the top three advances selected. In 2015, Greater Ground Resolution continued to be a primary concern; however, Greater Computer Processing Speed and Better Processing Software were the second and third most frequently selected trends. There was more diversity in the top selections for the 2015 technical advances than in 2010. The Software/Hardware sector chose Greater Computer Processing Speed, and the Academic sector chose Continued Increased Channels and Bands. These selections reflect the specific interests of each sector. For example, the ability to collect more channels and bands in the imagery would provide new opportunities for research in the academic world, while the software/hardware industry is focused on the speed and efficiency of its products. Based on the 1,547 survey responses, the Political, Economic, and Environmental trends that are likely to have the greatest impact over the next 10 years include National Defense/Homeland Security, Endangered Species/Natural Resources/Heritage Protection, and Global Warming. Some of these trends could have negative effects on certain sectors while having positive effects on others. It depends on whether the respondent is producing data and services or using data and services. For example, the increased interest in homeland security may result in restricted access data distribution, but the demand for data from the government will spur growth among data providers. The geographic comparisons between sectors indicated more pronounced differences in the Political, Economic, and Environmental trends than in the Technical Advances. Canada and the United States were most concerned about National Defense/Homeland Security, while the other sectors were split geographically between Remote-Sensing Data Becoming a Commodity, Required Cadastral Mapping, Expansion of the European Union, and Licensing Issues. Geospatial companies throughout the industry will need to take into consideration trends in all of the areas mentioned and assess for themselves how to best meet the needs of their domestic and international customers. Government and Commercial Usage of Data and Software Continue Upward Trend

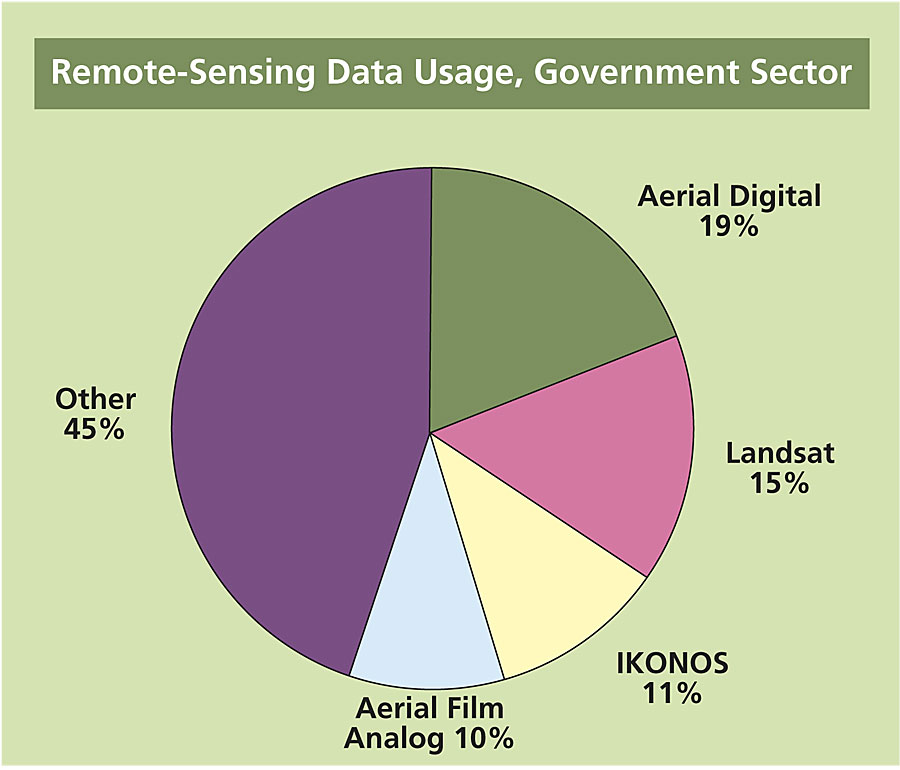

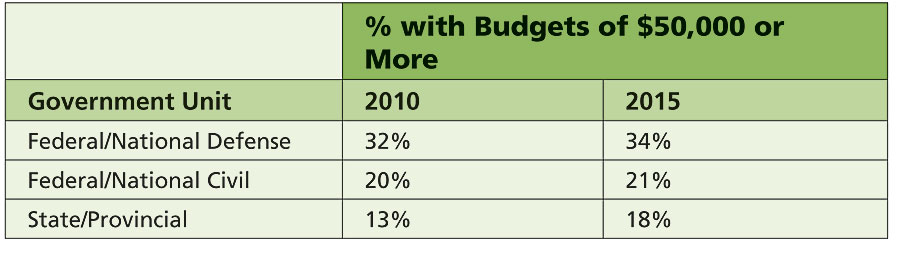

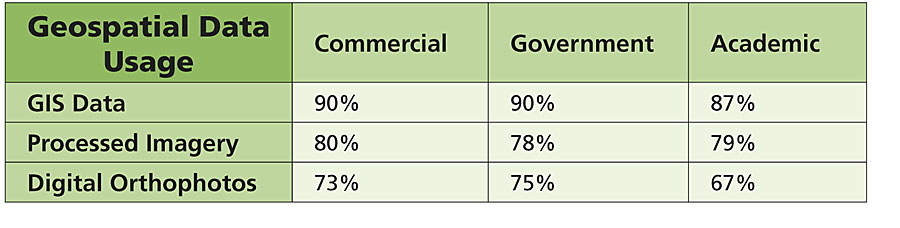

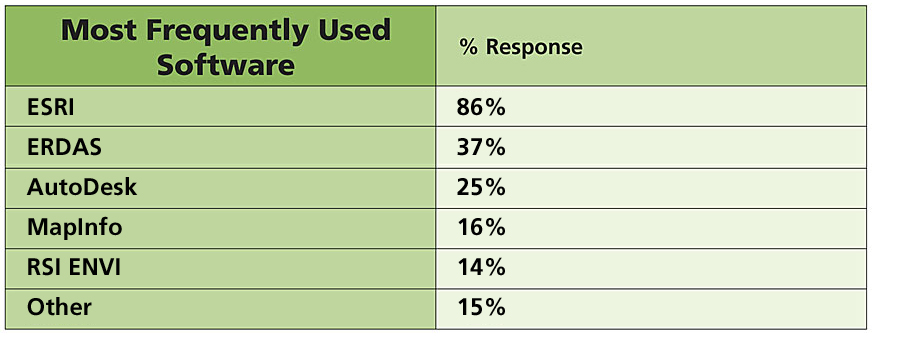

In 2010, 32 percent of Federal/National Defense respondents, 20 percent of Federal/National Civil, 13 percent of State/Provincial, and 18 percent of Local predicted budgets of $50,000 or more. There was a slight increase in budgets projected by 2015, with the most significant change predicted by State/Provincial respondents, which could represent the Canadian and United States governments' expectations for continued budget increases for Homeland Defense/National Security programs. To indicate potential demand for geospatial data, sectors were asked to select which types of data they use from more than 25 choices. Among the Academic, Government, and Commercial sectors, the top three types of data selected as most used were GIS Data, Processed Imagery, and Digital Orthophotos. These types of data are commonly used in a variety of GIS applications, such as municipal planning, vegetation analysis, and transportation management. The least-used types of data are Unprocessed Lidar and Unprocessed Hyperspectral, with usage percentages ranging from 11 percent to 22 percent in all the sectors. These findings are in line with the fact that these datasets are still somewhat new and processing lidar and hyperspectral data requires different training and technology. Raw imagery usage ranged from a high of 65 percent (Academic) to a low of 45 percent (Government). Unprocessed imagery is more appropriate for use by academics in research, while government employees are more likely to purchase processed data to use in their project applications. In responses about software preferences, Esri was clearly the software of choice, not only for the Government End User sector but also in all sectors and in all geographic areas. Esri response rates averaged 87 percent across all sectors and 86 percent among government end users. Strong Growth Predictions in All Remote-Sensing Sectors

The companies in the Aerial Digital and Aerial Sensor sectors overall selected larger revenue levels than Aerial Film and Satellite. By the year 2010, the Aerial Digital and Aerial Sensor sectors project an increase in market demand for their products and services, as indicated by increasing revenue and employee projections. The international market is a key market for the Satellite sector. In 2005, 22 percent of the Satellite sector respondents selected the international departmental category of "greater than $5 million" in revenue, and 30 percent of the respondents selected the international company revenue category of "greater than $5 million." However, the Aerial Digital sector projects an increase in international activity, so by 2010, its percentages of high-earning departments and companies are similar to those of the Satellite sector. Future Technology Impacts and DevelopmentsThe ongoing challenge in the remote-sensing industry is to make high-quality data accessible to more users—for an affordable price. The use of maps, aerial photos, and digital aerial and satellite imagery has already evolved dramatically during the past three decades�from primarily scientific and academic applications to commercial use in the media and on the Internet. Widespread consumer application of geospatial data has evaded the remote-sensing industry thus far, but there are several technology developments that have the potential to broaden the access and use of geospatial data. NOAA focused part of its analysis on the impact of related geospatial technologies on the remote-sensing industry over the next 10 years with 250 personal interview respondents selecting the following top three impacts. One way of increasing the supply of remotely sensed data is through increased use of microsatellites. Until recently, remote-sensing satellite programs were thought to be too expensive for most developing countries (India being the major exception). However, advancements in microsatellite technology have made the cost more affordable, and a growing number of countries are acquiring their own satellites, many through technology transfers or collaborative agreements with academic research institutions in other countries. Developing countries benefit from the less expensive access to remote-sensing assets. It is a matter of national pride to have a space program and allows workers to be trained to establish a new high-tech industry while also providing some independence from foreign data sources.

Remote-sensing technology developers have also refined the use of the spectrum to expand detection limits in wavebands, spectral resolution, and spatial resolution. Spectral imaging involves dividing the electromagnetic spectrum into narrow spectral bands, primarily in ultraviolet; visible; and shortwave, midwave, and longwave infrared. Multispectral imaging provides few bands, hyperspectral more bands, and ultraspectral many bands. Spectral imaging data allows extraction of features not detectable in conventional imagery. As developments in hyperspectral and advanced imaging technologies continue, they are likely to yield a cross-fertilization of technologies that will also find their way back into the traditional remote-sensing arena. As part of the entire imaging science field, remote sensing can be expected to continue to grow and expand its overall customer base as these technologies are incorporated and new applications emerge from their use. Just in the past few years, the value of remotely sensed data has been recognized by several heavy hitters in the Web services/search industry. Microsoft and Google, with combined annual revenue of more than $42 billion, have developed online mapping services called MSN Virtual Earth and Google Earth, respectively. The competition to capture the loyalty of consumers through fast, easy, up-to-date keyword searches linked to geographic data and maps has advanced awareness and demand more than any other trend recently. Others, such as Yahoo! Maps, have also recently entered the lineup to provide online mapping services. Microsatellites, hyperspectral and advanced imaging, and online mapping services are just a few of the technological improvements focused on broadening the access to and use of geospatial data. Combining improved data capabilities and lower-cost data with mapping tools that are more user-friendly is essential for demand to grow outside of the traditional mapping market and will thereby help increase the size of the entire remote-sensing industry. Remote-Sensing Research to Focus on Asia

"With so much business activity now occurring in the entire Asian region, it is a wise decision for NOAA to expand the remote-sensing survey to include Asia," says Kay Weston, chief, Satellite Activities Branch. The online survey, which can be completed in less than eight minutes, is posted at www.empliant.com/NOAA-remote-sensing-research. The survey respondents should be individuals involved in the remote-sensing industry within Asia or specifically doing remote-sensing-related business in Asia. Additional research network partners are being sought to host the survey Web site link on their sites and to initiate e-mails to their Asian databases encouraging respondents to complete the surveys. Research network partners will be recognized in all the material relating to the study and will receive the first release of the study in January 2007. Countries targeted by the survey include Australia, Bangladesh, Bhutan, Brunei, Cambodia, China, Hong Kong, India, Indonesia, Japan, Laos, Malaysia, Mongolia, Myanmar, Nepal, Philippines, Russia, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, and Vietnam. Esri Business Partner Global Marketing Insights, Inc. (the NOAA contractor responsible for the study), will collect online surveys through fall 2006 when data analysis will begin. The final report will be prepared and delivered to NOAA in late 2006. As with the current study, the results will be made publicly available. More InformationThe 74-page full NOAA-sponsored final report, "Survey Analysis of Remote Sensing Aerial and Spaceborne," from which this article has been extracted, is posted as a PDF for downloading by the public at www.licensing.NOAA.gov or www.globalinsights.com. Stop by the Global Marketing Insights booth #1614 at the 26th Annual Esri International User Conference to receive a free CD of the report and to complete the current Asian remote-sensing survey. Dr. Shawana P. Johnson, president, Global Marketing Insights, will be presenting a paper focused on additional study results on Tuesday, August 8 at 2:30 p.m. For more information about being a research network partner for the Asian study and for more information about custom analysis of the existing research data, contact Sherry Loy, Global Marketing Insights (tel.: 216-525-0600, e-mail: sherryloy@globalinsights.com). |